{kind=link}

How are mortgages different than typical loans, and why would you need a mortgage payment calculator?

Table of Contents

- What Are Mortgages for Homebuyers?

- How to Calculate Your Mortgage Payments

- Mashvisor’s Mortgage Calculator – What Makes It Better?

- Bottom Line

A mortgage calculator is a tool that every real estate investor needs to use to make calculations and predictions about their investment. In this article, we will explain everything you need to know about mortgages and their types, how mortgages are calculated, and what makes Mashvisor’s mortgage calculator the best option for you.

What Are Mortgages for Homebuyers?

Mortgages are basically loans that were designed for homebuyers. However, the difference between a standard loan and a mortgage is mainly in the requirements and specifics of the loan.

There are a number of money lenders in the US that specialize in lending money to homebuyers. Each lender imposes its own criteria and requirements to qualify for a mortgage. What they all have in common, however, is that they all specialize in real estate financing. It includes financing in order to purchase a primary residence or buy investment properties.

Below, we will go over the different types of loans that you can expect to find in the US, according to the type of lenders, the structure of the loan, and its duration.

Types of Mortgage Lenders

There are two ways to categorize mortgage loans. The first way is to separate mortgage types based on the lender and qualifications needed to borrow the money. Based on this categorization, there are two main types of mortgages that you can expect to find:

1. Conventional Mortgages

As the name suggests, it is the most common type of mortgage loan. Conventional loans are not backed by the federal government, which means private lenders offer them. There are two types of conventional mortgages:

- Conforming mortgage: This type “conforms” to the set of standards placed by the FHFA, such as factors about the borrower’s credit score and debt level.

- Non-conforming loans: This type does not meet FHFA standards, which means they are more flexible and are used by borrowers who have gone through financial issues such as bankruptcy.

Pros and Cons

As you would expect, there are advantages and disadvantages to using conventional mortgage loans.

For example, conforming loans have a strict limit on the size of the loan. As of 2022, the limits on a conforming loan are $647,200 in most markets and $970,800 in the more expensive areas. However, conventional mortgages tend to have lower overall costs than other types of loans, even though their interest rates are generally higher.

On the downside, conventional loans have stricter credit score requirements, which are often 620 or above. They also have higher down payment requirements than government loans.

Overall, conventional loans are good options if you’re looking for income properties for sale and you have a high credit score and the money to make a sizable down payment.

2. Government-Insured Mortgages

Unlike the previous loans, government-insured mortgages are provided by one of the three US government agencies: the Federal Housing Administration (FHA), the US Department of Agriculture (USDA), and the US Department of Veterans Affairs (VA).

Each of these departments provides its own type of mortgage loan to US citizens who qualify for that type of loan.

- FHA mortgage: This type of home loan is designed to help first-time homebuyers buy a property without being subjected to strict requirements, such as those by private lenders. The FHA loan will typically require a credit score of 580 to get the maximum of 96.5% financing, which means you only need to pay a 3.5% down payment with that credit score.

- USDA mortgage: This type of loan is provided to homebuyers who wish to own a property in a rural location that is within the USDA-eligible areas list. USDA loans may not require a down payment if the borrower has a low income.

- VA mortgage: This type is provided to current members of the US Army, veterans, and their families. It does not come with a down payment requirement or mortgage insurance.

Pros and Cons

While each of these types of mortgages has its own pros and cons, government-backed loans have certain advantages. It is generally easier to qualify for a government loan than for a conventional loan. Additionally, the credit score requirements for these mortgages are much more relaxed and don’t require a large down payment.

However, they also come with several drawbacks. The biggest disadvantage of government-backed loans is that they may require mortgage insurance premiums, especially in the case of FHA loans.

In addition, the loan limits on an FHA loan are lower than conventional loans, which will limit the inventory that you can potentially buy from.

Overall, it is trickier to use a calculator for a government-backed loan that has mortgage insurance on it since it is an extra cost that you will need to factor in.

Types of Mortgages – Interest Rate Payments

The other way to distinguish types of mortgages, especially when using a calculator, is to do so based on the loan’s interest rate over its lifetime.

Before moving on, it is important to point out that the duration of a loan can be decided by the lender, but most typical mortgages come in terms of either 15 or 30 years.

When it comes to the types of interest rate payments that real estate mortgages offer, there are two types that are very common:

Fixed-Rate Mortgages

A fixed-rate mortgage has a fixed interest rate over its lifetime. It means that the interest rate at which you take the loan will not change for the entire duration of the loan, and the monthly payments you make will always stay the same.

This type of loan is the easiest to calculate when planning for an investment, and it can be easily calculated with a simple mortgage calculator. However, the downside of this loan is that it will generally have higher interest rates than the second type of mortgage.

Since 30-year fixed-rate mortgages are very common, the interest you would incur over such a prolonged duration can be substantial.

Fixed-rate loans are popular among homebuyers who want to live in the property for several years and want to avoid potential changes to their monthly payments for that duration.

Adjustable-Rate Mortgage

In contrast, an adjustable-rate mortgage has a monthly payment plan that may change over the loan’s lifespan.

Typically, the interest rates will increase or decrease depending on the market conditions. However, most mortgages of this type will have a fixed interest rate for a set duration at the start before the rate changes at specific intervals.

For example, an adjustable-rate mortgage may have a fixed interest rate for the first seven years, and then it would start adjusting its interest rate every six months until the end of its lifespan.

Generally, this type of mortgage is considered somewhat risky, as the interest rates can increase beyond what you can afford in the long run. However, since the overall interest rate is lower than a fixed-rate loan, investors often prefer an adjustable-rate mortgage.

Many strategies that revolve around refinancing, such as the BRRRR strategy, will often prefer adjustable-rate mortgages because you can practically avoid paying higher interest rates by constantly remortgaging before the initial period ends.

How to Calculate Your Mortgage Payments

Now that you know what the different types of mortgages are, let’s talk about how a mortgage is calculated. When calculating the amount of monthly interest rate, the calculation is pretty simple:

You divide the annual interest by 12, and you multiply by the mortgage amount to get your monthly interest rate.

For example, if your annual interest rate is 4%, your monthly interest rate would be 0.33% (0.04/12 = 0.0033).

However, when calculating the monthly mortgage payments, things get complicated. Even for a fixed-interest rate mortgage, investors typically use a simple mortgage loan calculator to get a quick result.

So, it is not surprising that other types of mortgages would require more sophisticated calculators to make the whole process easier for homebuyers and investors.

Why Investors Need a Mortgage Calculator

Finding a good calculator all depends on the type of info that you want to get. For example, a mortgage amortization calculator will tell you how long it will take for your mortgage to amortize, and that will be the central angle of the output that it provides.

However, a mortgage payoff calculator will also need to have enough options to include all types of mortgages. The more you can customize the tool and the more input it allows you to give, the more accurate the results will be. It is mainly because most types of mortgages involve additional costs that homebuyers can often forget, such as insurance costs and taxes.

Of course, if you use a mortgage calculator with taxes, it will have to account for your location and the taxes that may apply to your specific case.

With all that in mind, there are many different calculator tools online; each has advantages and disadvantages. But if you’re looking for a platform that includes a calculator and will also help you find income properties for sale, we have the right tool.

Mashvisor’s Mortgage Calculator – What Makes It Better?

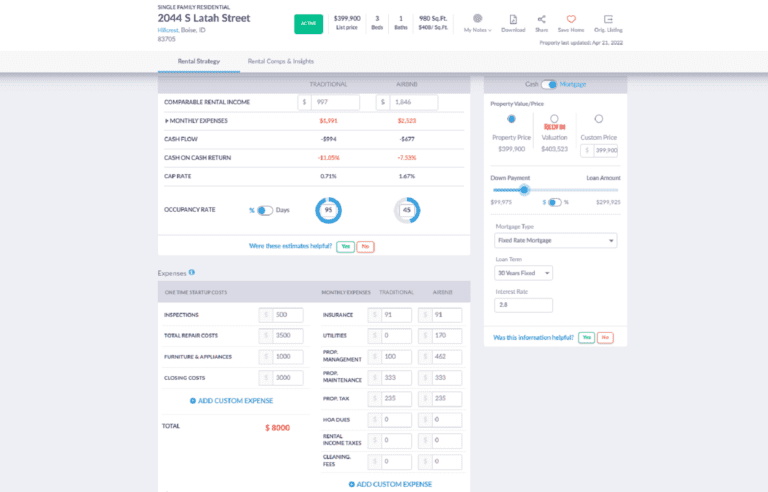

Mashvisor is a real estate platform that can help investors find an investment property based on actual data and analytics. The platform provides all the tools you need, including a mortgage calculator and a rental property calculator that accounts for your mortgage payments.

It means that, besides helping you find the best place to invest in real estate, the tool will calculate the return on investment that a rental property will have after calculating your mortgage payments.

By using real estate investing metrics such as the cap rate and the cash on cash return, the tool can significantly reduce the amount of time needed to analyze the long-term outcome of investing in any rental property.

Mashvisor’s mortgage calculator will provide the return on investment from a rental property after calculating your mortgage payments.

A Flexible Mortgage Calculator

Unlike other calculators, Mashvisor’s calculator allows you to choose the type of mortgage that you want to use. It includes fixed and adjustable-rate mortgages, and you can pick a 15- or 30-year duration.

While the fixed-rate option acts as a simple mortgage calculator, the adjustable-rate calculation is quite complex to be done by hand. Since the tool is connected to the rental property calculator, any input you make in the mortgage section will immediately be reflected on the property’s analytics page. It includes the rate of return on investment, the monthly expenses related to owning the property, and the long-term payback analysis of your investment.

All of the above features make Mashvisor the best when it comes to analyzing your purchase before making it.

Mortgage Calculator: Calculate Monthly Payments

Investing in real estate is indeed a lucrative endeavor. It offers the investor generous profits, a steady income, and property they can use for leisure.

Although cash transactions are ideal, most real estate investors still choose to apply for a mortgage. The only thing is they have to incorporate mortgages into their ROI and revenue calculations.

Fortunately, they now have the chance to calculate how much their payment will be even before they invest in the property. It is a huge help in their careers, which brings numerous advantages.

Mashvisor’s mortgage calculator allows investors to calculate their monthly payments. With this investment tool, decision-making is made simple.

To learn more about the significance of this calculator, how to use it, and more valuable tips regarding your investment property, scroll down.

How to Calculate Your Monthly Mortgage Payment

Although the ideal would be to purchase the property with out-of-pocket cash, many investors choose to apply for a mortgage. It requires the investor to focus on several different factors affecting further action.

Here is a brief step-by-step guide on how to start your calculation:

Step 1: Determine Your Mortgage Principal

This is the amount you borrowed from the lender, which you’ll have to pay back. For example, if you apply for a fixed-rate mortgage, you’ll have uniform monthly payments until it is fully paid.

Step 2: Calculate Your Monthly Interest Rate

This is a fee that the lender charges you for the borrowed money. If you’ve maintained a high credit score and can pay a larger down payment, you’ll score a lower interest rate.

Step 3: Calculate the Number of Your Monthly Payments

If you apply for a fixed mortgage rate, you’re looking at either 15 or 30 years. A 30-year mortgage requires 360 monthly payments, while a 15-year mortgage requires 180.

Step 4: Decide on Private Mortgage Insurance (PMI)

This is a type of mortgage insurance you’ll need if you pay less than 20% of the purchase price upfront. The PMI premium will be added to your monthly payments.

Step 5: Consider Property Taxes

Don’t forget that your monthly mortgage payments include property taxes. These will be collected by the lender and allocated to an escrow account.

Step 6: Consider Homeowner’s Insurance

If you’re applying for a mortgage, there is a high likelihood that you’ll be required to pay for homeowners insurance. There are different types of this insurance policy, so consult with the insurance company.

Step 7: Use a Mortgage Calculator

Considering the complexity of the calculation, you should find a reliable mortgage calculator to help you decide on the loan duration, warn you if you’re spending beyond your budget, and so on.

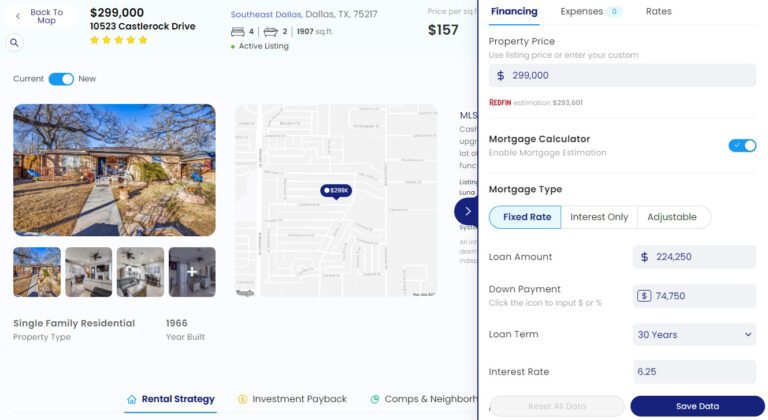

How to Use Mashvisor’s Mortgage Calculator

It’s time to introduce you to the tool that will save you time and energy when calculating monthly mortgage expenses.

Mashvisor’s Mortgage Calculator is specifically designed for the needs of investors like you.

It assists you in estimating the costs that come with the investment property in question. This tool will show you all the vital metrics within minutes. You can factor in anything: property taxes, insurance premiums, HOA fees, annual percentage rate, and so on.

Our calculator relies on up-to-date analytics and verified data.

Investors can also customize the result based on the term and type of mortgage they applied for. They consult with their lender first to find the most appropriate mortgage type:

- Fixed-rate mortgage

- Adjustable mortgage

- Interest-only mortgage

To explore the full advantages of Mashvisor’s features, sign up now.

Mashvisor’s Property Finder tool has a built-in mortgage calculator to make computing much easier for investors.

The Significance of Calculating Monthly Mortgage Payments for Investors

Before developing a strategy, you should be aware of monthly mortgage payments.

Although some advantages are clear, it’s helpful to outline them again, especially for beginner investors just entering the market.

Financial Planning

Regarding the significance of mortgage payment calculation, the first order of business goes to finances and establishing a budget before you invest in a real estate property.

In short, everyone is aware that monthly mortgage payments are inevitable monthly expenses for an extended period. And you must be ready to pay it and set the ground rule–the budget.

With business endeavors like this, it is essential not to get carried away and to stay within your financial limits.

If an investment property seems like a one-time opportunity, but your financial situation does not allow it and exceeds your budget, our friendly advice is to keep searching.

Return on Investment (ROI)

Besides using the investment home loan calculator to determine your financial flexibility and possibilities, it is imperative to pay attention to another critical factor—the ROI.

Your mortgage payments will hugely influence your return on investment.

Briefly, this is one of the crucial investment metrics used to evaluate the profitability of an investment compared to the price. More precisely, it measures the profit gained from the investment.

It is generally expressed in percentages. Here is the formula:

ROI = (Net Profit ÷ Cost of Investment) x 100

For reference, net profit refers to the total gain from the investment venture.

Risk Management

Lastly, when calculating the monthly payments for your investment home loan, it’s crucial to consider the risk factor.

Simply speaking, relying on a mortgage calculator predetermines their monthly payments and clarifies the recurring expenses (insurance, homeowners association fees, and taxes, among others). It helps real estate investors better understand the risk of the investment.

It brings us back to the first point. If the investment is too risky, it’s a clear warning sign that you might need to search for an alternative.

What Costs Do You Need to Prepare for as a Prospective Rental Property Investor?

If you’re a prospective real estate investor, you must know the potential costs that await you before you come to terms with them. As far as real estate investing goes, here are five unavoidable costs:

Purchase Costs

First and foremost, you must be prepared for purchase costs. This group implies:

- Down payment – the upfront payment

- Closing costs – appraisal fees, title insurance, legal fees, etc.

- Inspection costs – general and pest inspection, specialized assessment

Mortgage Payment

Among all costs, your monthly mortgage payment is the biggest and the most important one. These recurring expenses will be with you for a long time. Bear in mind that your monthly mortgage payments include principal and interest amounts.

Insurance Premiums

Real estate investors will also have to pay private mortgage insurance. As with other mortgage payments, PMI protects the lender and not the investor.

Paying PMI is usually associated with conventional loans, where the investor makes a down payment lower than 20% of the property’s purchase price.

Property Management Fees

If you are planning on hiring a property manager, you must take into account the fees associated with that. Property management fees are a percentage taken from your monthly income.

How Much Income Do You Need to Qualify for a Mortgage as an Investor?

There’s no denying the fact that real estate properties imply much higher financial requirements.

First, your lender will require a minimum of 20% down payment. The main reason is private mortgage insurance (PMI) does not cover investment properties.

Note that some lenders might even require 25% for the down payment. This might be the case if you’re considering investing in two- to four-unit apartments with a 620+ credit score.

Be prepared to supply the lender with additional paperwork. They will most likely want to see two to three years of your income tax returns.

Here’s a more detailed overview of what lenders will look into:

Proof of Income

Lenders will want to see that you have a stable income.

For instance, if you have recently changed jobs, the lender may require a letter from your employer proving your income. You could also use investment income dividends and interests to qualify.

Be prepared to submit more documents.

Credit Score

Real estate investors considering conventional mortgages will need a credit score of at least 620. Higher credit scores can secure lower interest rates, while higher interest rates compensate for additional credit risk.

720 is a good credit score, while 760 and above is considered excellent.

Loan to Value Ratio (LTV)

The loan-to-value ratio (LTV) presents the maximum amount a lender will finance you for a property relative to the property’s appraised value. It’s a measure of the risk your lender is taking on. A higher down payment means a lower loan-to-value ratio and a lower mortgage payment.

Debt to Income Ratio (DTI)

The debt-to-income ratio (DTI) compares how much you currently pay in debts monthly to how much you earn each month. In essence, this represents what percentage of your income goes towards debt payments.

Now that you have a general idea of what lenders will be looking into and some major financial requirements on your side, it’s time to prepare you for the investment property hunt.

What Makes a Good Property Investment?

To close off today’s topic, we’ll look at some factors that make an investment property a viable option for real estate investors.

1. The 1% Rule

Generally, the 1% Rule states that the rental income should be at least 1 percent of the purchase price. Conversely, this means you don’t buy a property with a price greater than 100 times the expected rent. It’s a good rule of thumb for many investors.

2. Occupancy & Vacancy Rate

Occupancy rate is the percentage of occupied units compared to total units in space. Beyond the individual property metrics, the occupancy rate measures how profitable your location is. It can be a test of market hotness or coldness. Areas with high occupancy rates signify high demand because people are moving there, while a high vacancy rate in an area is a red flag.

To get a good idea of the desirability of a place, look at how vacancy/occupancy rates have changed in recent times.

3. Cap Rate

Cap rate measures the potential return you can expect within a year. It’s estimated by using the formula:

Cap Rate = (Net Operating Income ÷ Property Value) x 100

Calculating the cap rate is extremely important, and it’s one of the most commonly used metrics that helps you compare properties.

4. Cash on Cash Return

Cash on cash measures the cash yield of the property. If you’re financing your property through a mortgage, cash on cash return becomes a more relevant metric.

Note that cash on cash return focuses solely on cash inflow and outflow and doesn’t factor in property taxes. Cash on cash return is the annual pre-tax cash flow divided by the total out-of-pocket money used for purchase.

Here’s the formula:

Cash on Cash Return = Annual Pre-Tax Cash Flow ÷ Total Cash Invested

5. Expense Ratio and Debt Coverage Ratio

When comparing similar properties, you should take note of the expense ratio and the debt coverage ratio.

The expense ratio (ER) shows what percentage of your rent earnings go towards operational expenses. You should aim for a lower ratio. On the other hand, the debt coverage ratio focuses on the relationship between your rental income and your mortgage—how much of your total rental income goes towards mortgage payments.

Airbnb Rental Calculator

Bedrooms

Bathrooms

Bedrooms

Bedrooms Bathrooms

Bathrooms

Final Thoughts: Investment Mortgage Calculator

It’s not uncommon for real estate investors to apply for a mortgage when investing in a particular property. However, they are expected to fulfill specific requirements: down payments, closing costs, property management fees, and so on.

Mashvisor’s investment home mortgage calculator provides an easy way to be informed about the financial situation and the potential profit that can be generated if you decide to apply for a mortgage.

You can calculate the estimated monthly mortgage rates based on the type of mortgage you are applying for.

When searching for a lucrative investment property, factor in the 1% rule, occupancy and vacancy rates, cap rate, cash on cash return, and expense and debt ratio.

To start using our real estate investment tools today, sign up for a Mashvisor subscription.