{kind=link}

Buying a stock cooperative might sound like a lucrative investment strategy for diversifying a real estate portfolio, but is this really the case?

Growing a successful real estate business is all about expanding your collection of properties with new profitable opportunities at all times. If you’re in a major city where standalone buildings like single-family homes are prohibitively expensive, you might have been thinking about housing cooperatives.

Table of Contents

- What Is a Co-Op?

- Are Co-Ops the Same as Condos?

- How Do Stock Cooperatives Work?

- What Are the Pros and Cons of a Stock Cooperative as an Investment Property?

- How to Invest in a Co-Op

- Can You Borrow Money to Invest in a Stock Cooperative?

- Can You Earn Rental Income Through Co-Ops?

- Should You Invest in a Stock Cooperative?

However, before getting your feet wet in any kind of investment, you need to know what you’re getting yourself into and what it entails. You want to check if it will be worth the capital investment, the risks involved, and the potential return on investment.

The same applies to co-ops. You should be aware of what these are, how they work, how to invest in them, and whether they might be beneficial at all. Today, we will provide in-depth insight into co-ops and help you assess whether they are worth investing in. We’ll also show you how Mashvisor can support your investing decision.

Related: Condo vs Co-Op: Which Is the Better Real Estate Investment?

What Is a Co-op?

In real estate, a co-op refers to a housing cooperative, which is different from traditional homeownership or the ownership of a conventional investment property. In terms of the structure, a co-op is exactly what it sounds like – a residential property where the inhabitants who live in different units co-own the space.

Co-ops are usually not-for-profit. The main difference between investing in a property and investing in a co-op is that with the second, you don’t own a home. Instead, you become a shareholder in the corporation that owns the housing cooperative. Each shareholder is entitled to use a unit in the cooperative that corresponds to the size of their share.

The shares within the property are allocated depending on the units’ market value. The size of the apartment determines the owner’s co-op shares. The rest of the space is considered common areas.

Like any other cooperative, each co-op is run by a board of directors. The board is elected by the members to oversee the management and maintenance of the property. However, every shareholder retains the right to a say in how the property should be managed.

What Is a Stock Cooperative?

A stock cooperative is a residential apartment development where the undivided interest in the land is combined with the occupancy of an apartment unit. The idea is identical to a housing cooperative.

From an investor’s point of view, investing in a stock cooperative is more similar to investing in the stock market than in the real estate market. It is because you don’t buy a housing unit but co-op shares that give you the right to lease and reside in one of the units. The proprietary leases also give you the right to use the common areas of the cooperative.

While stock cooperatives might not be a very popular real estate investing strategy, they are not new. They’ve been around for decades, especially along the East Coast. Most of them are in New York City and various cities in the California housing market.

Are Co-ops the Same as Condos?

Many think co-ops are the same as condos because of shared ownership, common areas, and a management board. However, condominiums can be classified under traditional real property because once you buy a condo, you get a title to ownership. Condo owners benefit from all the advantages of possessing an investment property.

In short, when you purchase a condo, you gain outright ownership. You can use the property as collateral against a loan or decorate and renovate it in any way you wish, within the HOA’s regulations and restrictions. It’s relatively easy to secure financing to purchase a condo, as most loans for investment properties work with condos.

On the other hand, when you invest in a co-op, you’re buying shares in a cooperative that functions very much like a stock corporation. You might have a place to live but don’t own it. You can’t flip the property or easily resell it. Co-op owners are only asked to leave if they break co-op laws, but there is only so much they can do with their unit other than to occupy it.

When you finally leave, you relinquish your shares back to the cooperative. They are then given to the next person who becomes a member.

Co-ops are pretty restrictive regarding ownership compared to other real estate investment options. They have stringent requirements for investors willing to buy.

The application process involves an interview with the board before you get approval to buy co-op shares. Furthermore, though you don’t own your unit, you might be required to meet a particular net worth or debt-to-income ratio to show that you can meet the fees needed for upkeep and maintenance.

Also, importantly for investors, co-op units don’t generally allow subleasing.

How Do Stock Cooperatives Work?

A housing cooperative owns both the exterior and the interior of the unit. You’ll need to seek the board’s approval even for the slightest renovations, such as kitchen remodeling.

Once you invest in a stock cooperative, you’ll be required to pay a monthly fee that will go into facilitating the maintenance costs. Part of the fees may also go into paying the property’s mortgage.

One of the core values of co-ops is mutual responsibilities and financial obligations. Members split all costs, such as property taxes and utilities, in a ratio determined by each unit’s value. Thus, co-op owners should be ready to pay higher monthly fees than condo owners as the fees are more comprehensive. But they benefit from discounted rates typically available for higher-value purchases and services.

The board of directors is responsible for creating policies that are in the best interest of the co-op. These policies are commonly known as by-laws. For example, the board could pass a by-law for certain thresholds new shareholders must meet before approval. Most boards also pass by-laws that prohibit subletting.

Investing in a co-op limits the amount of equity you can own, if this is an option at all. There are three different types of co-ops when it comes to equity:

- Market Rate Co-Ops: These stock cooperatives allow shareholders to buy and sell shares at the market rate.

- Limited Equity Co-Ops: With this type of co-op, the board controls the rate at which members can buy and sell shares.

- Leasing Co-Ops: There’s no equity accumulation as the co-op leases the property instead of owning it.

What Are the Pros and Cons of a Stock Cooperative as an Investment Property?

Like any other investment, you need to have a deep insight into the advantages and disadvantages of stock cooperatives before deciding whether to put your hard-earned cash in them.

Here are the pros and cons of buying a co-op apartment for investment purposes:

Pros of Investing in a Co-Op

Many people, especially those living in big cities, choose to buy co-ops because they provide them with entry-level housing.

Below are the main advantages of investing in a co-op:

- Lower buying and closing prices: Co-ops are generally cheaper than condos and have lower down payment requirements. The closing costs are also lower since the title deed doesn’t change hands. You’re not required to pay transfer taxes.

- Minimal responsibility: Unlike owning a single-family home or a townhouse where you’re fully responsible for maintenance and repairs, you can take a backseat with co-ops. It’s more like renting, so you’re not in charge of management or maintenance other than your unit.

- Familiarity with the neighbors: You may not have an outgoing personality, but you’ll get to know a lot about your neighbors. All potential shareholders have to reveal enough about themselves for approval. While the board can reject an application on the basis of finances or character, they’re not allowed to do so based on race, religion, or other protected categories.

- Being heard: As a shareholder, you might not be on the board of directors. However, you still have a say on how the property should be run.

Cons of Investing in a Co-Op

Investing in a stock cooperative may already seem like an ideal investment for the reasons listed above. Nevertheless, there are a few things you need to consider before jumping in.

Here are some disadvantages of buying a co-op:

- High monthly fees: Co-ops might have lower purchasing and closing fees but higher monthly fees. The monthly rate is determined by what expenses need to be sorted out. In some cases, you may need to pay parking fees and various utilities.

- Restrictions: Always make sure you understand the terms before investing in a co-op since some boards are notorious for going overboard. Ensure you read the by-laws and understand what you may or may not do. For example, some may not allow you to repaint your unit, but they may make it easier to sell later on.

- Less liquidity: Co-ops have a limited pool of potential future buyers because of restrictions on resale. This makes them far less liquid than other forms of real estate investments and makes it hard to gain long term profit from appreciation.

- Restricted renting: If you’re looking for a rental investment property for sale, keep in mind that stock cooperatives are not the best option. In the majority of cases, the subletting of units is not allowed.

How to Invest in a Co-Op

Always do your homework beforehand and carefully review the legal and financial documents. Before you sign the contract, see how much repairs the unit needs and be sure about the potential for equity accumulation. If it’s possible, have a home inspection done on the unit.

Before you can invest in a co-op, you’ll first have to seek approval from the board. The board runs the same way as a homeowners association, deciding who’s supposed to live where and how the property should be run. You can meet up with one of the board members to get a feel of the association and determine whether you want to be part of it.

Most importantly, you need to get your credit in order and have a solid financial history. You’re trying to qualify for both the lender and board.

Another vital part of the process is conducting investment property analysis on the stock cooperative, including the entire building and the individual unit. The type and level of analysis will be dictated by what you plan to do with your investment co-op property, whether you want to use it as a second home or intend to rent it out. If you plan on the latter option, ensure that it is allowed.

Related: Are HOA Fees Worth It? A Guide for Property Owners

Can You Borrow Money to Invest in a Stock Cooperative?

Yes, you can get financing to invest in a stock cooperative. However, this is different from obtaining a loan to buy a standalone property as an investor.

Instead of a conventional mortgage, you can take out a share loan. With a share loan, the shares you own in the cooperative serve as collateral. Remember, you don’t get a title to show ownership of the unit, so you can’t use it as collateral.

Share loans may be harder to come by compared to traditional loans, but they’re available. Credit unions are usually the best lenders for real estate investors looking to buy co-ops. When you apply for a share loan, the lender will require information to understand how the co-op operates. They’ll also look into the board of management and see if there’s any underlying mortgage.

Some co-ops have established special arrangements with lenders to make financing for potential shareholders easier. So, make sure you check if this is an option in case you require financial help.

Related: 6 Best Companies Offering STR Loans

Can You Earn Rental Income Through Co-Ops?

Whether you can turn a stock cooperative investment into a rental property depends entirely on the by-laws of the co-op. In most cases, this is strictly prohibited, including both short term rentals and long term rentals.

Even if the board allows subletting, they may have certain measures in place to stipulate how long you can rent out a unit. For instance, there may be a two-year limit for renting out every five years. This may restrict the kind of leases you offer and the tenants you attract.

For those co-ops that allow you to use your unit as an income property, it’s common to find clauses that say you must have lived within the unit for a specific amount of time before you can rent it out. Tenants may also have to go through the same approval process as buyers. In addition, subleasing may involve additional expenses that you have to pay to the co-op or managing agency.

So, all in all, if you’re looking for a real estate investment property to rent out, do a lot of research and ask around before opting for a co-op apartment.

How to Maximize Rental Income from Your Stock Cooperative Investment

If you find a co-op where you can rent out your unit, you need to conduct a thorough rental property analysis to confirm if this is, indeed, a wise investment.

Instead of having to collect and analyze data manually, you can use the Mashvisor investment property calculator. This tool uses nationwide real estate data and proprietary analysis to tell you precisely what rental income, cash flow, and ROI you can expect. All you have to do is to enter the address and type of property you’re considering to get started.

Airbnb Rental Calculator

Bedrooms

Bathrooms

Bedrooms

Bedrooms Bathrooms

Bathrooms

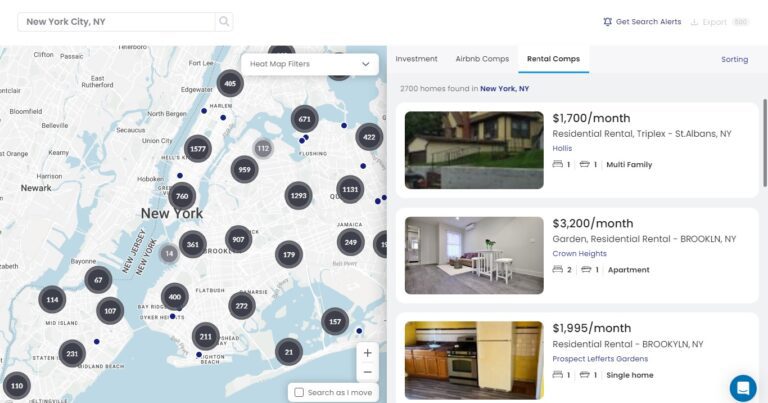

The analysis provided by the Mashvisor rental property calculator relies on rental comps or active rental listings similar to the one being considered. It includes all must-have numbers to make a profitable decision, such as:

- Operating expenses

- Rental income

- Cash flow

- Occupancy rate

- Cash on cash return

- Cap rate

The analysis is available for renting out both on a short term and long term basis. Moreover, all numbers and values are adjustable so you can customize your analysis for the co-op fees you’re expected to pay monthly. Like always, if you want to invest in a stock cooperative unit to rent out, remember to aim for positive cash flow and a cap rate between 8% and 12% from the beginning.

To start analyzing the investment potential of co-ops (or any other residential rental properties), sign up for a 7-day free trial of Mashvisor.

When you enter any location of your choice using Mashvisor’s Property Finder, you can access rental comps in the area for a more thorough investment property analysis.

Should You Invest in a Stock Cooperative?

Whether you should invest in a stock cooperative depends on your situation, goals, and aspiration.

You should ask yourself the following questions to know if investing in a co-op is the right move for you:

- What are your business goals?

- How do you intend to use the co-op?

- How much are you willing and able to spend on an investment property?

If you’re looking for something more pocket-friendly, co-ops might be your best option since they tend to be inexpensive. Generally speaking, this is a good option for those looking for a hedge against inflation to protect their savings.

However, consider the fact that you’ll have to work hard to get approval from the board, and you might need to work with a lender you haven’t worked with before if you need financing.

Also, remember that co-ops tend to be harder to sell. The seller is responsible for the transfer fee, which is about 3% of the selling price. When you factor in broker/agent fees, transfer taxes, and other miscellaneous closing costs, you might end up spending up to 10% of the proceeds from the sale.

If you’re looking for property to give you immediate cash flow, co-ops may not be the best option for you. But they could be great if you want a place to call your own in the city or rent after living in it for some years. You could also buy one if you have a child going to college in that city and will need a place to stay for a few years.

Key Takeaways

A stock cooperative could be a great investment option for investors looking to buy real estate. However, they are different from any other form of real estate investing, offering their own pros and cons as well as having specific requirements. Like any other investment opportunity, you need to do your due diligence to evaluate whether a co-op is a suitable strategy for you.

Get your finances in order, talk to the board, ask for a copy of the by-laws, review the legal documents, and conduct rental property analysis if you plan to sublease. Remember that Mashvisor can provide all the help that you might need with this last part. Our investment property calculator helps you check if any property in the US residential market is a good opportunity for you before you buy it.